|

What are the best investments and where will I generate the greatest return, which areas of the market are the most attractive, what products should I buy, and which providers should I use? Headlines, conversations and reading material are often centered around investment returns. These are all valid questions and certainly very relevant. While investment returns take center stage in conversations, it is only one side of the coin. The other side of the coin, that is often neglected, is your savings rate. For money to grow, it needs to be there, and saved, in the first place. The magic really happens when you combine saving and investing, we could call it the “The Ultimate Power Couple”

0 Comments

Novice investors are often overwhelmed by some of the jargon investing professionals use, to the point where it can feel almost like listening to or reading a foreign language. There's no Duolingo edition that translates financial "industry-speak" to English (at least, not yet), but the following glossary is a start. Of course, this is just the tip of the iceberg, and new investing terms come into vogue all the time. But at a minimum, the terms defined below should serve as a starting point for novice investors or those who are sometimes left scratching their heads after reading a fund manager's quarterly message.  The South African Revenue Service (SARS) has announced significant updates for the 2024 tax season, including provisions for solar energy and tax-free savings. The new tax season begins on 1 July 2024, with the introduction of auto-assessments. SARS has outlined six key changes for individual taxpayers, involving updates to processes, forms, and tax categories. These changes primarily address technical details, such as the timing of deductions for contributions to retirement funds and tax-free savings accounts, as well as the introduction of new subsidies. Notably, the 2024 tax year marks the implementation of the solar tax credit, and individuals who have utilized this temporary subsidy should ensure it is properly declared this year. You can read more here from SARS regarding the Tax season, SARS Tax Season. Key filing dates  Please take note that previously some auto assessments received by our clients required corrections and adjustments, so don't just simply accept SARS' assessment. Review it and consult a tax practitioner if you need help. You may contact our Su-Chin Chen who is our Accountants by sending an email to: [email protected] Tax CertificatesYou should have received tax certificates from financial institutions in last few weeks to aid in your tax filing. These certificates include those from medical aids, banks, life insurance companies, and investment companies. Please check your email inbox and junk folder, searching for the keyword "tax certificate" to locate relevant emails. Download the attached tax certificates and save them in a folder on your local drive or cloud storage for your tax filing purposes. Below we indicate how you can get your tax certificate from Various providers:

Discovery Health

If you would like assistance with getting your tax certificate please contact our team on email: [email protected], tel: (011)658-1333 For our investors investing in Morningstar Managed Portfolios, click below to access the latest performance snapshot, market commentary and market performance summary:

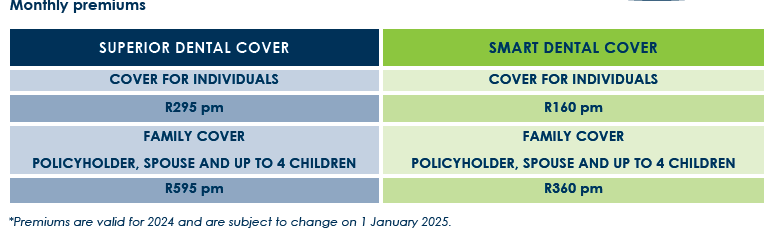

Morningstar SA Managed Portfolios Morningstar Global Managed Portfolios (USD) Market Commentary - SA and Global Market Performance Summary - SA and Global Last month we shared with you about Zestlife - Dental Cover and on May 2024 Zestlife has updated the product options. We share with you about the product offerings. What is Dental cover Dentistry Cover is a health insurance policy that is designed to assist individuals and families to fund the high cost of private dentistry. This innovative dental insurance pays a stated amount for your general dentistry, emergency, accidental and illness-related dental treatment costs. The two options: Superior Dental Cover: Provides funding for a comprehensive range of dentistry treatment costs. High stated cover amounts* are provided to fund in part or whole, the actual costs of general, emergency, accidental, illness related and specialised dental treatment. Smart Cover: Provides more affordable funding for frequently incurred dentistry treatment costs. This option pays lower stated cover amounts* to fund in part or in whole, the actual costs of general, emergenc y, accidental and illness related dental treatment costs. The Superior and Smart Cover options are both suitable for individuals and families on medical aids that provide limited or no dental cover. Dental Cover is not a medical aid and the cover is not the same as that of a medical aid. This policy is not a substitute for medical aid me membership. *The stated benefit amounts are the total benefit to cover the costs relating to the diagnosis, subject to the terms and conditions of the policy. Who is covered? Cover is available to you as an “individual” as the only life insured or to you and your immediate family. The family option includes cover for yourself, spouse and children as well as grandchildren. To qualify for cover a grandchild must be a dependant on your medical aid. SPOUSE is the person to whom you are married by law, tribal custom or tenets of any religion. Only one spouse can be covered under the policy. CHILD(REN) means your child or children, legally adopted children, stepchildren under the age of 21 or older if they are physically or mentally handicapped and dependant on the parents for financial support, or your grandchildren provided that they are dependants on your South African medical aid. A maximum of 4 children may be covered on the policy. Click here for full brochure If you would like to apply for dental cover, contact Amber in our Health department email: [email protected],tel: (011)658-1333   Many clients are asking the question, “Now that the National Health Insurance is signed into law, do I cancel my medical aid?” The short answer is “No”, as the NHI will take at least three years to set up its systems and infrastructure.

The NHI Bill, a landmark piece of legislation, aims to transform the healthcare landscape in South Africa. There are multiple concerns including the quality of the legislation, the constitutionality of the Bill and the processes followed during the adoption of the Bill. The market seems to estimate that the signing of the NHI Bill is an “industry-specific risk” (pricing in of higher policy uncertainty regarding the longevity of private medical schemes in South Africa) and not a risk for the entire economy. Implementation and Funding The implementation of the NHI will be phased over several years to ensure a smooth transition. The first phase will focus on strengthening the existing public healthcare system and expanding access to primary healthcare services. Subsequent phases will involve the gradual integration of private healthcare providers and the establishment of the NHI Fund. Reactions and Challenges The NHI Bill has garnered mixed reactions from various stakeholders. Proponents argue that it is a crucial step towards achieving social justice and improving public health outcomes. They emphasize that the NHI will help reduce health disparities and provide financial protection against the high costs of medical care. However, critics have raised concerns about the feasibility of the NHI, particularly regarding its funding and implementation. Some fear that the transition to a single-payer system could be fraught with administrative challenges and inefficiencies. There are also concerns about the potential impact on the private healthcare sector and the quality of care during the transition period. Will it affect your medica aid? Adrian Gore the Group Executive of Discovery explains very well the impact of NHI to the medical aid industry. "People are concerned about the continuity of their cover in its current form. We understand this concern. It is based on a component of the Act - Section 33 - which is problematic. Section 33 states that once NHI is ‘fully implemented’ medical schemes will be able to cover only those services that are not covered by NHI. This implies that medical scheme cover will be replaced by the NHI at that point in time. While this appears threatening, practically it isn’t. This, for two reasons. First, the impact of Section 33 is that only once the NHI is ‘fully implemented’ will medical schemes be limited in the cover they provide to medical scheme members. Until this point, there will be no change to your medical scheme cover. We believe it will take a long time – a decade at least – to achieve ‘full implementation’ given the scale and complexity of reforms needed. Bear in mind the NHI is an inordinately large and complex initiative that proposes extraordinary change and restructure to public and private healthcare systems. This is unprecedented and will be incredibly difficult to achieve. Second, even when the NHI is ‘fully implemented’, medical schemes will still be able to provide cover for benefits not covered by the NHI. This is important because the NHI is unlikely to have sufficient funding to provide an extensive package of benefits. This is because our country unfortunately faces significant financial constraints linked to low economic growth and a very narrow tax base. Medical schemes will therefore still play a significant role post full implementation of the NHI." Click here to read the full response In summary, your medical aid benefits will continue to exist, but there may be changes in how they operate alongside the NHI. It is essential to stay informed about updates from both your medical scheme provider and the NHI developments to understand how these changes might affect your coverage. 2024 is a big year on the election front, with democracy taking center stage. With more than half of the world's population heading to the polls, it’s understandable that investors are feeling a sense of unease. Elections tend to bring up a lot of emotion, introduce uncertainty and prompt investors to brace for some market volatility. Couple this with the geopolitical tension that is already persistent. |

AuthorKevin Yeh Archives

January 2025

Categories

All

|

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

-

I would like to

- Signup Newsletter

- Schedule an appointment

- Go to hospital

- Deal with an accident

- Make a Claim

- Invest >

- Apply for insurance >

- Appoint Daberistic as broker

- Promotions >

- Update my policy >

- Make a Will

- Set up a business

- Get an accountant.

- Get business tax advice

- Get personal tax advice

- Preferred Suppliers >

- Cancel Daberistic Services

- Covid-19 toolkit

-

Invest

- Our fund selection process

- Retirement annuity

- Tax-free Investment Plan >

- Unit Trusts

- Guaranteed Investments >

- Preservation funds

- Offshore

- Education plan

- Endowment

- Participation Bond

- Deposits

- Business investment accounts

- Private investment accounts

- Exchange Traded Funds

- Share investing

- Personalised share portfolio

- Retirement income

- Retirement Funds

-

Health

- Life

- Insure

-

Financial Coach

-

Accounting & Tax

-

About us

-

我想要

- 财富管理

- 员工福利

- 人寿保险

- 医疗保险

- 财产险

- 会计师事务所

- 关于我们

RSS Feed

RSS Feed

Services |

About us |

Support

|